Headlines

- Weaker BNSF car freight trade

- Front end PNW corn and soybean basis slightly weaker

- Gulf corn/soybean basis weaker; domestic corn/soybean basis firm

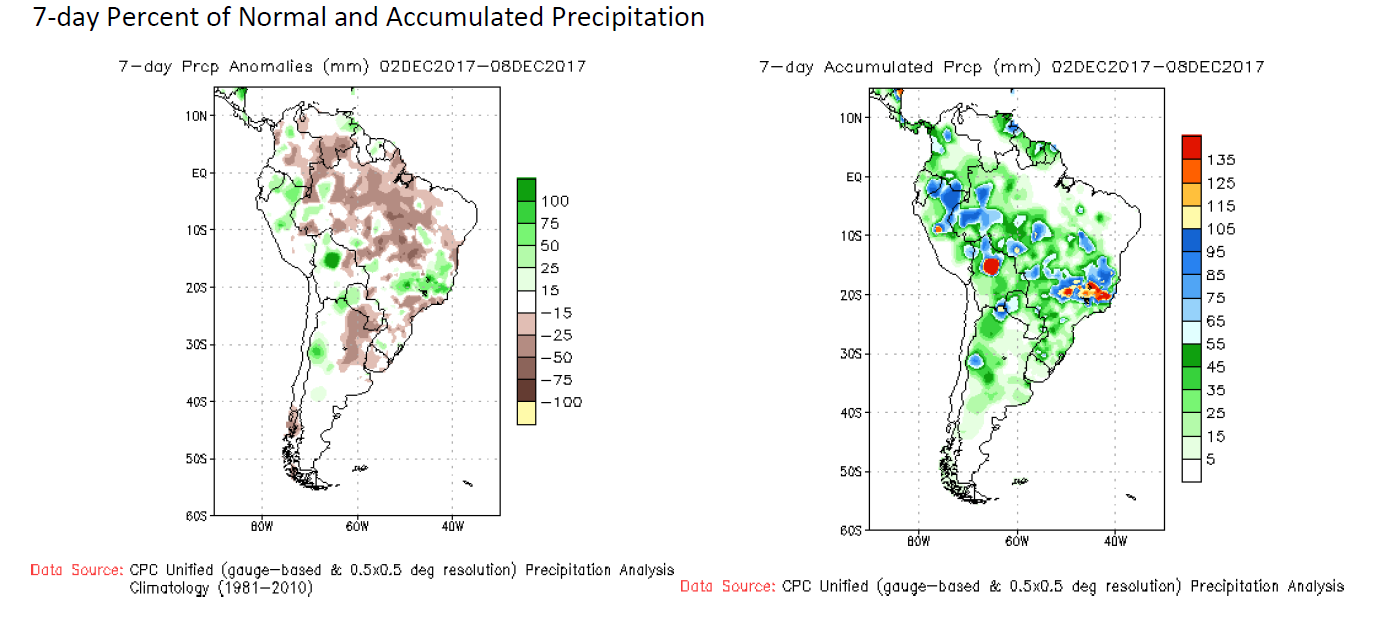

- Argentina weather turned a bit wetter

Pre-report Estimates and Polling for 2017/18 Market Year

Corn

- US ending stocks 2.478 bb vs 2.487 LM (better ethanol prod; HAS to include lower yield?)

- Global ending stocks 202.72 mmt vs 203.86 LM

Soybeans

- US ending stocks 438 mb vs 425 LM (weak exports; my bias is above 438mb)

- Global ending stocks 97.82 mmt vs 97.90 LM

Wheat

- US ending stocks 938 mb vs 935 LM (weak exports)

- Global ending stocks 267.07 mmt vs 267.53 LM

Exports

Exports continue to be challenged in this environment. Corn sales were 34.5 mbu compared to 29.9 mbu last year at this time (There were 60M bu weeks on each side of this value last year). We are still missing those corn sales to China which were all the buzz 2-3 weeks ago. Soybean sales were above expectations at a lofty 74.1 mb, helping to get us more on track. Hopefully sales weeks like this will continue, but with the real falling apart again this past week it’s hard. For the third straight week we’ve seen very weak spring wheat sales (1.6 mbu) and it’s very concerning. Things can turn around quickly in this wheat class so stay tuned. I expect a sleepy market to continue until SAM weather is straightened out or export pick up against the typical seasonal pattern in Jan.

Domestic Demand

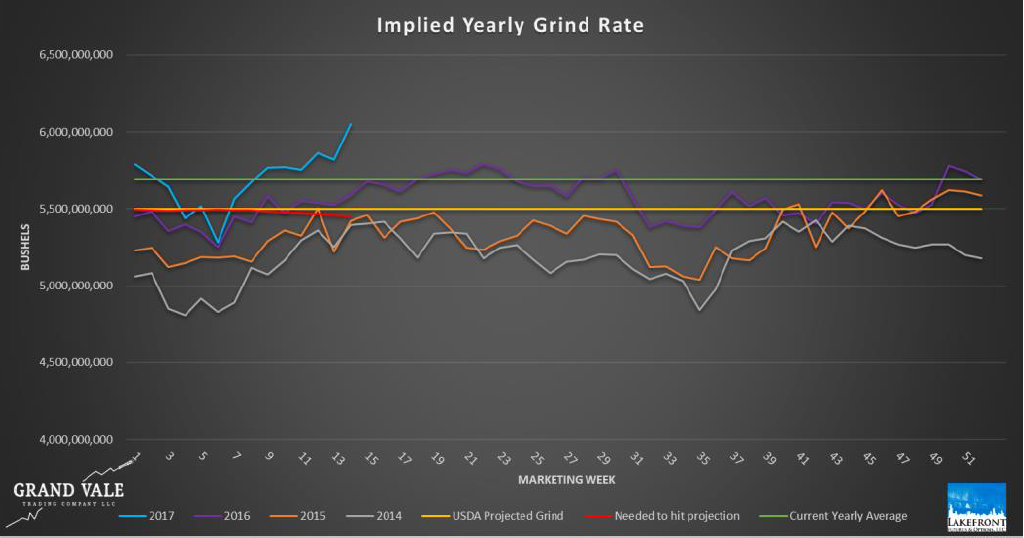

Ethanol producers ran at a blistering rate the week prior at 1108k bpd compared to 1066 the week prior and 1023 last year. This helped to bring on a stock build of 500k barrels and a 1-day blow to ethanol margins of a few cents per gallon. I expect that producers will continue to run hard through the end of the year and am hopeful that industry participants were able to step past emotion and greed and lock unseasonably good margins for Q1. Soybean crush margins improved over the week prior. Soybeans crushed in October were 176 million bushels versus 145 million in September and 176 million in Oct 2016.

South America

The focus continues to be on dryness in Argentina and Southern Brazil while Brazil chugs toward another huge crop. Mid-week the GFS turned wetter for Argentina over the next 10-14 days and soybeans lost their grip. We can’t allow ourselves to focus entirely where the rest of the market is and forget about the other main players. There will be significant output from South America and in my opinion the reduced production will likely be focuses on second season corn in Brazil more so than soybean production. This should help improve the corn picture over time especially when China comes back into the picture as a world player and it sure “feels” like that could be within a year or two. We need to keep an eye on this closely as this is likely the most supportive thing in the market right now and IF it leaves there isn’t much left until spring potentially giving us that buyback opportunity on beans below 950 futures that we are looking for. In order for this plan to be effective we need to make sure that the size of short positions is significant enough to earn “needle-turning” premium.

Commitment of Traders

Technicals

The chart below again references the spot corn futures and is known as a continuous chart. On it are fairly long-term moving averages, trend lines, Fibonacci retracement lines, and slow stochastics. I like using these tools alongside some fundamental intuition for making longer term projections for price and trends. You can see that the now deliverable Dec contract (the spot month) has been finding support for a third time just over 336. The concern here is that Dec rolls off next Friday and then leaves little protection for March to begin trading down into the 335-345 zone we’ve become accustomed to for the spot month. In addition, we can also see that a descending trendline remains intact that began in August. While the weekly chart has a higher low than the week prior I’m very reluctant to pick a bottom here.

Continuous Soybean Chart

Soybeans have shown a lot of respect for the standard retracement levels on the chart as you can see by the chart above. January beans have been unable to hold values above $10 for any length of time, however, they have been getting bought around 986. January beans broke the trend line to the downside on Thursday and confirmed that move on Friday.