Jack Finfer joined Lakefront Futures/aiSource in 2022 as a Research Analyst and in 2025 was promoted to VP of Operations.

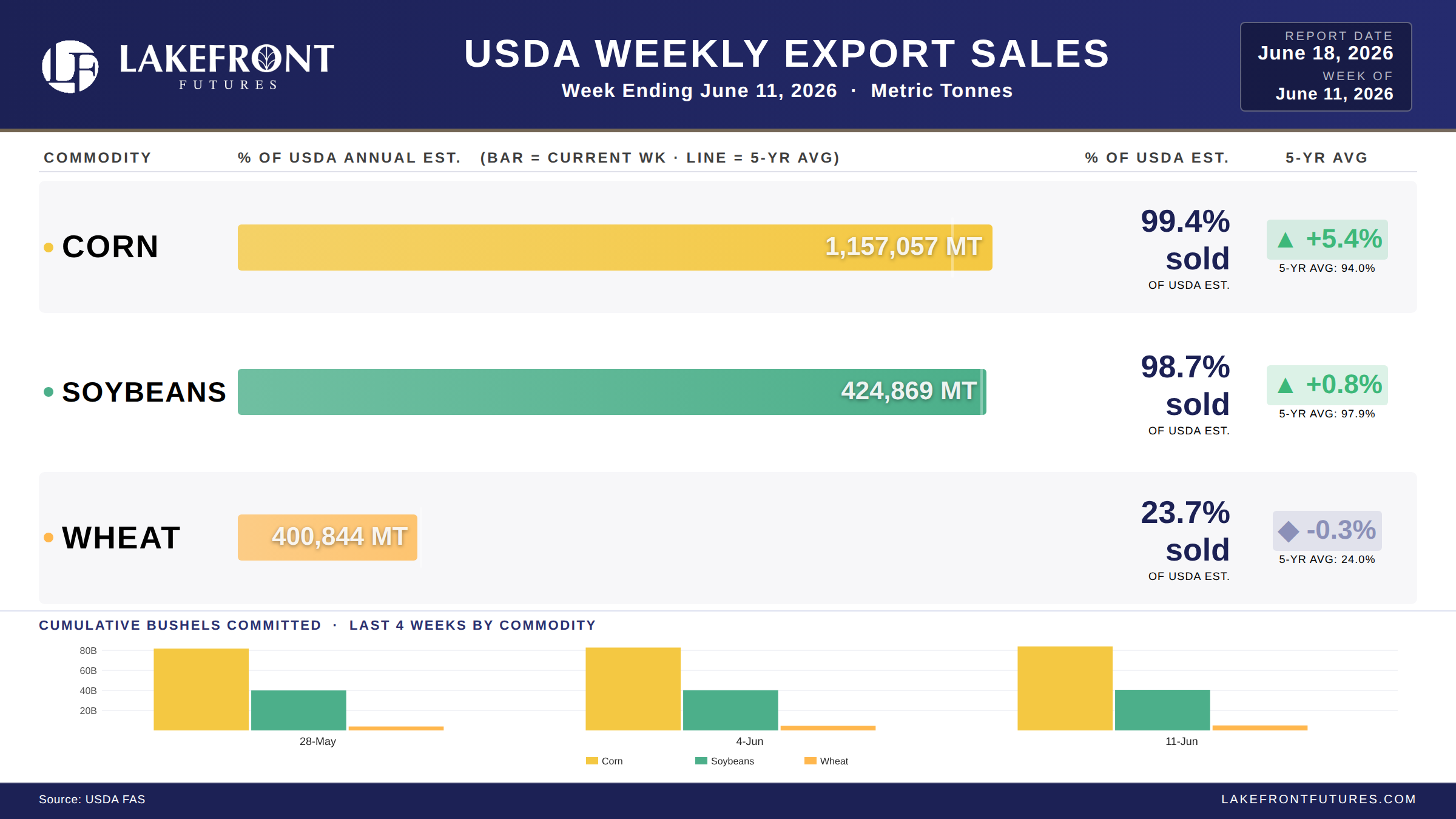

Jack runs the Lakefront Futures Briefing, covering every major USDA and EIA government report release with charted analysis on cattle, grains, energy, and export data.

Jack works alongside Lakefronts managed future division, aiSource. He manages aiSource's CTA database, handles account opening and back office operations, and works directly with CTAs and CPOs on trade execution and clearing. His responsibilities include client onboarding, returns reporting, listing maintenance, and ongoing operational support for all clearing clients. Jack also conducts strategy research and due diligence on new CTA programs for the aiSource database.

Originally from the north suburbs of Chicago, Jack studied Entrepreneurship and played football at Illinois Wesleyan University. Outside of work, he enjoys sports, fishing, and spending time with family.