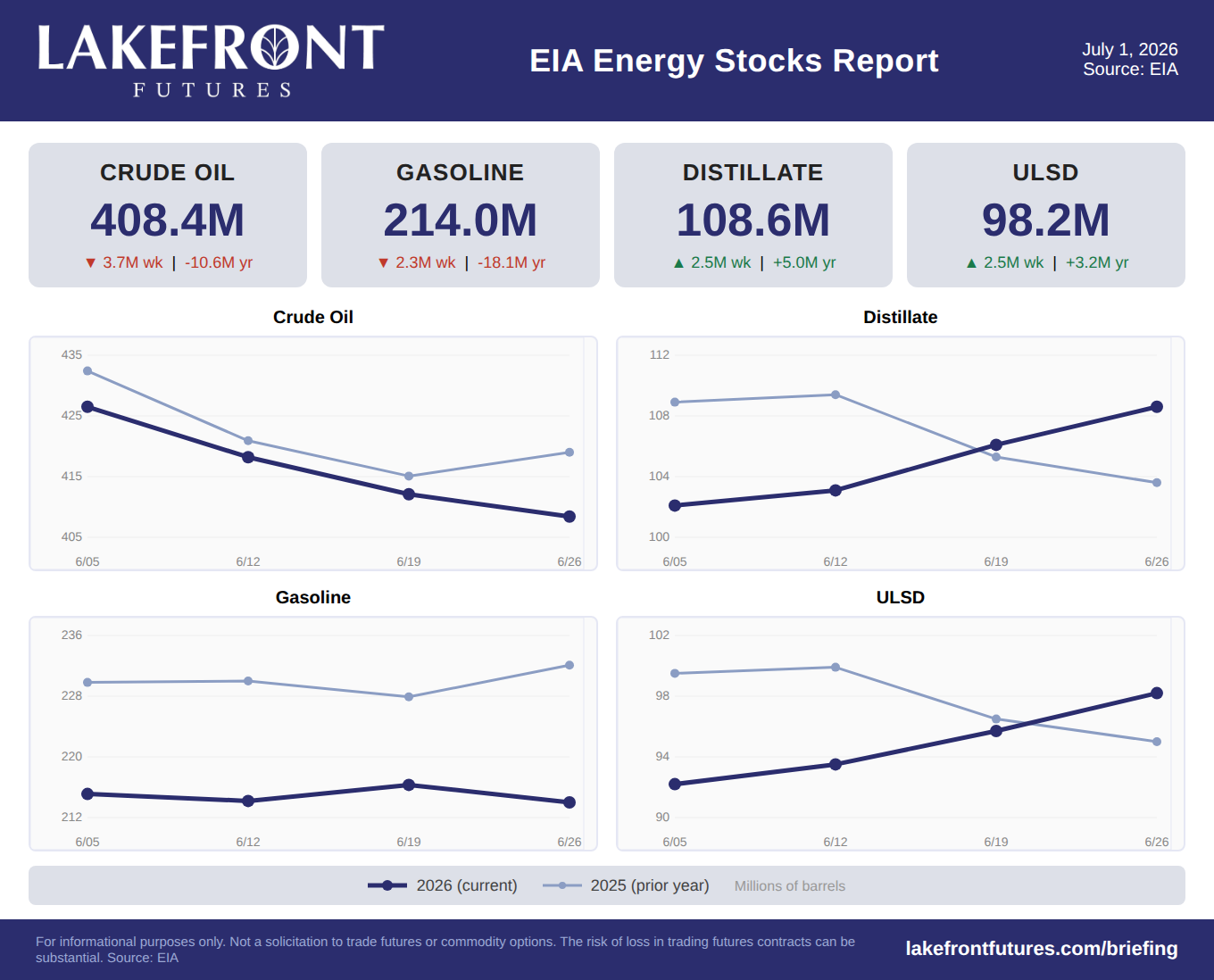

Crude and gasoline both drew this week, down 3.7M and 2.3M barrels respectively, while refineries pushed utilization to 96.6%. The dual draw is notable in the context of the massive year over year deficits now in play: crude sits 10.6M barrels below last year and gasoline is a striking 18.1M barrels light. Distillate and ULSD built 2.5M each, but the product side is not where the tension is. WTI settled Friday at $69.23, having crashed through its 200 day moving average at $73.76 and printing an RSI of 15.4, deeply oversold territory that historically sets the stage for at least a technical bounce. The 20 day swing low at $68.56 is the immediate floor, and a failure there exposes the mid $60s. Heating oil at $3.21 remains above its 200 day near $2.94 with RSI at 34.5, while RBOB at $2.96 is holding well above its own 200 day at $2.42 with RSI at 43.5, suggesting the products are weathering the crude selloff better than the flat price would imply.

With the Strait of Hormuz open and Middle East barrels gradually returning to market, the supply side is normalizing. But the inventory data tells a different story: the U.S. is burning through crude and gasoline faster than supply can replenish, and the EIA’s June STEO projects Brent easing only to $89 by Q4 even with restored flows. At $69 WTI, the market appears to have overshot the fundamental picture to the downside.

|